Private equity (PE) has been a constant, and growing, phenomenon in corporate finance over the last three decades and its importance is likely to increase in the post-Covid world as firms will find headwinds after the removal of the many government support programs introduced in 2020.

One industry that has received significant attention from PE funds is the healthcare industry, including hospitals. Perhaps because of the nature of hospitals and their centrality in the provision of healthcare, it is not surprising to witness substantial controversy surrounding the presence of PE funds in this field. Those more favorable to PE funds argue that these investors provide hospitals with much needed funding to invest in new technologies that should ultimately improve patient care and health outcomes. Those who oppose PE funds in this industry claim that the usual behavior exhibited by these investors in other industries – such as higher debt, selling of assets, and layoffs to generate profits – will lead to a negative impact on communities’ access to health care and lower jobs.

Janet Gao, Yongseok Kim, and Merih Sevilir examine this important issue from the point of view of employment, efficiency and patient outcomes at hospitals in their paper “Private Equity in the Hospital Industry”. They compare these outcomes in hospitals acquired by PE acquirers with, first, a sample of non-acquired hospitals, and then, hospitals acquired by non-PE acquirers.

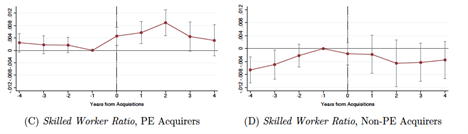

Janet, Yongseok and Merih find that total employment at target hospitals acquired by PE funds significantly declines after acquisition. On the brighter side, the proportion of skilled workers in such acquired hospitals, namely physicians and nurses, in the total workforce increases for hospitals acquired by publicly traded PE funds. These results have to be contrasted with what happens in the case of hospitals acquired by non-PE investors: employment cuts also occur, but skilled worker ratio does not increase in those hospitals. These outcomes, and their magnitudes, can be easily discerned from the graphs below which show how employment and the presence of skilled labor have changed around acquisitions (year 0) made by, separately, PE and non-PE acquirers.

Figure 1: The Figure shows how employment changed in hospitals acquired by PE funds (Panel A) and those by non-PE acquirers (Panel B) after the acquisition (year 0).

Figure 2: The Figure shows how the ratio of skilled workers (physicians and nurses) over total employment changed in hospitals acquired by PE funds (Panel C) and those by non-PE acquirers (Panel D) after the acquisition (year 0).

Perhaps because of the higher presence of skilled workers in PE funds-acquired hospitals that the authors also observe another important finding: patient satisfaction scores do not decline at PE-acquired hospitals and even improve along some dimensions after such acquisitions. Also, PE acquirers are not associated with higher mortality and readmission rates at target hospitals compared to non-PE acquirers.

This research provides new evidence on the role of PE acquirers in the hospital industry and paints a more nuanced picture with the differences between PE and non-PE acquirers, as well as between PE-backed acquirers with and without access to public capital markets.

Leave a Reply